Through +ACTion, the Fluid Ice Foundation is spreading awareness about essential financial inclusion public policies in the US.

The financial inclusion gap has always been existent, and the COVID-19 pandemic further highlighted these disparities, as many people relied on digital payments, credit cards, and other financial tools, which many of the un/underbanked did not have access to. It is essential for both policymakers and the business community to work together to address challenges and impediments to reaching the underserved communities, and bring combined perspectives on community needs and impact through public policies. As part of our digital advocacy efforts, we have identified key/illustrative public policies in the US for financial inclusion, that you can learn more about to help improve and support financial inclusion.

Key Ways to impact Financial Inclusion through Public Policies

1

Literacy

In the US, only 11 states have public policy requiring 15+ hours of financial literacy instruction in high school (less than 38% of all high school students nationally). States where public policy requires financial literacy in high school, have increased correlation with financial well-being. The potential for increased financial literacy & inclusion, will be huge, if all states/countries globally incorporated public policy to promote earlier access to financial literacy.

2

Awareness

Public policies can and have been introduced to require research into the impeding factors for financial inclusion and spread awareness (i.e. Financial Inclusion in Banking Act of 2021), to discover possible solutions. For example, special committees can be created to specifically research and analyze why more people are not included in the financial system and what would be the best solutions, or surveys of the masses, to drive insights in shaping financial inclusion public policies.

3

Credit Unions

Credit Unions/Community Banks are essential to serving their communities, however, many are overshadowed by larger counterparts, & unable to keep up in this constantly changing world and provide services to those who need it most. The number of credit unions in the US is decreasing: in the last 10 years, decreased from around 7,000 to 5,000. It is key to ensure credit unions/community banks have tools & regulatory environment suitable to their development.

4

Competition Policy

A market open to fair competition helps by incentivizing the expanse of the range of products and services and increased efficiencies/quality of service and lower costs, which ultimately means potential consumers currently on the sidelines will be more easily included. The number one cited reason for being unbanked is not having enough money due to the high fees and account minimums required to be able to participate in/use financial institutions.

5

Digital Equity

Digital equity public policy to support sustained efforts to eliminate the digital divide as a barrier to economic and educational opportunity is essential. In the US alone, more than 9 million children lack internet access at home for online learning. Especially with the proliferation of FinTech and the shift to online learning in schools due to COVID-19, Digital Equity has become more of a necessity and a priority now than ever.

6

Social Justice

Social Justice, including racial gaps, gender gaps, wealth gaps, access to education, and access to the basic necessities of life, are important for enabling financial inclusion. Research shows that racial inequities have cost the US a staggering $16 trillion in the last two decades, and if racial gaps were closed today, $5 trillion could be added to the US GDP over the next five years. You cannot get healthy and wealthy on your own – societies make progress, not individuals.

Key/illustrative public policies in the US for financial inclusion, that you can learn more about to help improve & support financial inclusion.

Financial Inclusion in Banking Act of 2021

To amend the Consumer Financial Protection Act of 2010 to direct the Office of Community Affairs to identify causes leading to, and solutions for, under-banked, un-banked, and underserved consumers, and for other purposes.

To improve the financial literacy of secondary school students by directing the Department of Education to award competitive grants to state educational agencies and, through them, subgrants to local educational agencies to integrate financial literacy education into public elementary or secondary schools.

A bill to amend title 39, United States Code, to provide that the United States Postal Service may provide certain basic financial services, and for other purposes, and has the power to set interest rates and fees for the financial instruments and products provided by the USPS.

A bill to require the Assistant Secretary of Commerce for Communications and Information to establish a State Digital Equity Capacity Grant Program, and for other purposes, for promoting digital equity, supporting digital inclusion activities.

To establish programs and requirements related to minority banks, Black banks, community banks, women’s banks, and low-income credit unions, by providing regulatory relief, to codify the Minority Bank Deposit Program, and for other purposes.

To amend the Small Business Act to optimize the operations of the microloan program, lower costs for small business concerns and intermediary participants in the program, and for other purposes.

Want to learn about several additional financial inclusion public policies?

We have created a representative list & repository of key US state-wise and national public policies, to help you learn more about and support financial inclusion initiatives.

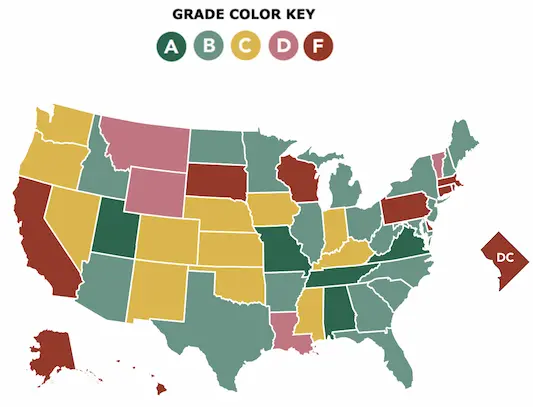

Champlain College's Center for Financial Literacy, using national data, has graded all 50 states and the District of Columbia (D.C.) on their public policy efforts towards requiring financial literacy in high schools.

Grade A: State requires 60+ hours of personal finance instruction in all of high school Grade B: State requires some personal finance instruction - around 15 hours in all of high school Grade C: State has personal finance topics in its academic standards, but no oversight by the state Grade D: State has very little personal finance instruction requirements, with low implementation Grade F: State has virtually no personal finance instruction requirements

Only five states earned an A, with Utah having the best personal finance requirements in high school of the five states.

Just 11 states require 15 or more hours of personal finance education in all of high school – 22% of all the states in the US, which account for only 38% of all public high school students, with the rest receiving less than 15 hours of personal finance education.

27 states were classified under grades C, D or F, and 30% were classified under grades D or F.

Non-contiguous states (Alaska & Hawaii) both received an F classification for little to no personal finance requirements in high school.

Two states appear to have made a surprising reversal:

In August 2016, Idaho revised their economics course standards and as a result, the number of hours of personal finance instruction estimated by the study dropped from 11 hours to 7.5 hours of instruction.

Louisiana is the only state since the 2008 financial crisis that has materially reduced personal finance education standards for high school students. Louisiana offers but no longer mandates/requires students to take personal finance instruction, causing Louisiana’s grade to drop from Grade B to Grade D.

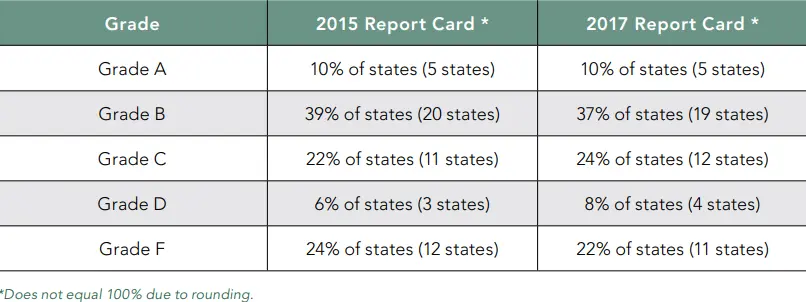

Over the years, there has been slow but steady progress regarding the teaching of financial literacy in our nation’s public high schools. However, what the grading shows is that we still have a long way to go before we are a financially literate nation.

States with better personal finance education requirements are more likely to have high school graduates with a better understanding of managing money and a better overall financial well-being.

Does your state have effective financial literacy public policy?

Thirty-seven states, Guam, Puerto Rico and the District of Columbia have addressed financial literacy legislation in 2022. Some examples:

Washington provided student financial literacy education; provides that the financial education public-private partnership shall establish a grant program to provide assistance to school districts for the purpose of integrating financial literacy education into professional development for certificated staff.

Michigan amended the Revised School Code to beginning with students entering grade 8 in 2023, to require students to complete a course in financial literacy (per requirements in the bill) to receive a high school diploma, and required the Department of Education to develop a half-credit course in personal finance.

Delaware, Michigan and Rhode Island declared April 2022 as Financial Literacy Month in the state.

Raj Mehta is the Founder and CEO of the Fluid Ice Foundation. As a high school student in the Atlanta metro, Georgia, Raj always enjoys helping others, and aspires to give back to society at every opportunity that comes along. Raj is particularly passionate about financial inclusion, to expand access to financial services to the un/underbanked subsets of the population. Although the un/underbanked subsets of the population have always been excluded, the recent COVID pandemic has made it even more apparent, and caused them to be even further left behind. Raj sees himself as a “social impact catalyst” and a “changemaker” to help mitigate the financial divide, and he aims to make this a reality through his nonprofit – Fluid Ice Foundation. Raj is also a CFEI Certified Financial Education Instructor helping increase financial literacy awareness and education, especially amongst the underprivileged youth.

Raj is focused to be a social impact entrepreneur/innovator, championing sustainable innovation by transforming societal assets/capital to enable disruptive solutions providing a positive return to society.

On a more personal note, Raj enjoys mathematics and has won numerous prestigious math competitions (qualified to Mathcounts Nationals to represent the State of Georgia, AIME, AMC, etc.), is a proficient saxophonist (member, Georgia Music Educator’s Association (GMEA) Allstate Band), is an advanced chess player, and a professionally trained/skilled golfer. He is also an avid book reader in his spare time.

Vijay is the Banking and Capital Markets Leader for Deloitte South Asia. He has over 25 years of consulting experience spanning strategy, business planning, organizational transformation and M&A in India, as well as in Canada, the UK and South East Asia. Among other topics in banking and capital markets, he has significant experience in fintech solutions and related partnership models.

Vijay is also a founding team member of I_Imagine_India, an India-based philanthropic fund looking to empower non-government organizations and social entrepreneurs/pioneers in the field of education in India. I_Imagine_India’s goal is to enable small changes today in the field of primary/ pre-primary education, with the potential to deliver disproportionate learning outcome improvements over the longer term.

Vijay obtained an MBA from the Indian Institute of Management, Ahmedabad (PGPX) and the Chartered Financial Analyst (CFA) charter from the USA.

Vijay is an Advisor to the Fluid Ice Foundation in his personal capacity and not on behalf of Deloitte or I_Imagine_India.

Saiprasad Muzumdar, Advisor

Saiprasad ‘Zoom’ Muzumdar, is an experienced Senior Technology Leader in International Banking and Finance Sector. He has a Bachelor’s degree in Engineering and a Master’s degree in Management. He has worked across the globe for International Fortune 500 companies such as Unisys, Citigroup, Lehman Brothers, Nomura, Royal Bank of Scotland/NatWest Group. He has conducted sessions on Financial Wellbeing for more than a decade with a mission to enhance financial inclusion and financial wellbeing through Financial literacy.

Amit Pandit, Advisor

Amit is a qualified chartered accountant with over 25 years of experience in banking, financial services, capital markets, risk advisory services & financial education. He has experience in building a primary market distribution network, investment banking and handling HNI relationships. He has been involved in personal finance restructuring of many individual businessmen. He has helped many business and individuals for their financial requirements be it for loan arrangements or debt management or asset management. He served as a director of the largest coop bank in India for over 13 years and as a director of a listed company for over 5 years.

He is also associated as a visiting faculty with various business schools for over a decade and takes up subjects of Personal Finance Planning, Wealth Management, Mergers & Acquisitions & Corporate Valuation. He also takes corporate training programs for finance. He speaks at various platforms on various finance, audit and risk related topics including ICAI, BCAS etc. Amit looks after the business building, financial & investor education function at Trugrow.

Amit enjoys his reading, is passionate about his teaching, likes travelling and exploring new destinations and is an avid foodie.

We use cookies to ensure that you have the best experience on our website. If you continue to use this site, we will assume that you accept this.OK